In the ever-evolving landscape of real estate investments, despite worries about escalating expenses and an economic downturn, the U.S. retail sector has experienced stable growth in 2023 due to several factors.

The U.S. retail real estate market is experiencing its tightest conditions ever recorded, with about 4.7% of retail space available. Over the past year, retail availability has decreased by 50 basis points and is nearly 200 basis points lower than its historical average of 6.8%. Minimal availability of retail space and a lack of new supply, which mitigates the potential increase in store closures, contribute to the stability of retail fundamentals. Additionally, as construction costs and occupancy have increased, landlords are able to improve rents better than they have in the last 3-5 years.

Retail’s resilience also lies in the fact that e-commerce constituted approximately 15% of overall retail in Q1 2023. Simply put, customers can’t obtain everything online. Many services still strongly prefer or even necessitate in-person visits, including barbershops, nail salons and restaurants.

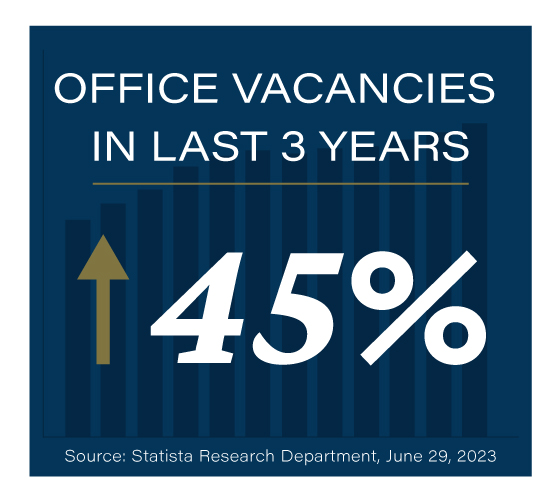

After taking a hit at the onset of the COVID-19 pandemic, CRE has been on the mend. According to the International Monetary Fund, prices of residential and industrial properties have surged globally since the end of 2020, while the retail and multifamily sectors have shown signs of stabilization. Office investing carries the highest risk out of the primary CRE sectors due to high vacancy rates and reduced demand.

The bottom line? Retail should be a foundational allocation of your portfolio. Over time, real estate investment has become less risky and more profitable. Retail was the only asset class to experience significant year-over-year volume growth in 2022, while most others exhibited double-digit declines.

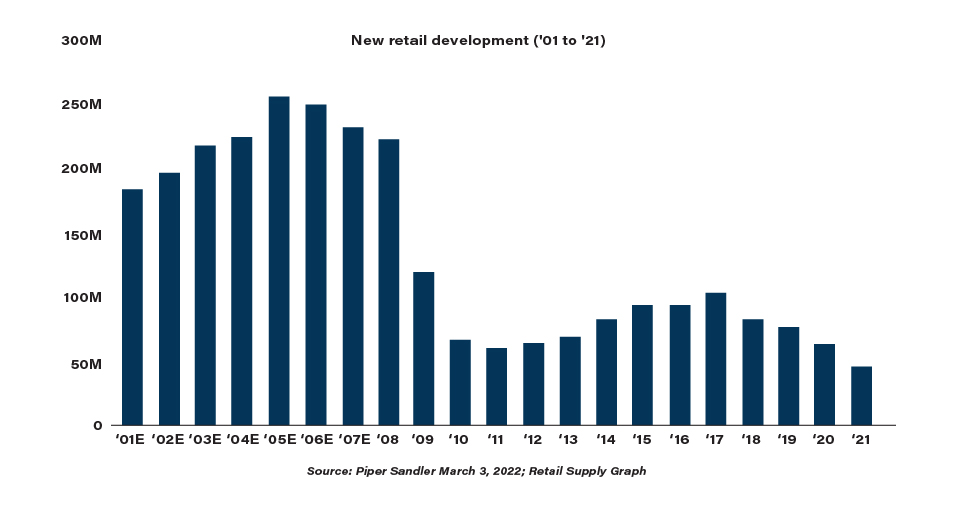

The upsides of retail real estate are relatively lower risk and an improving retail climate. Over the past 13 years, there has been a historically low amount of new retail development. In fact, the retail sector remains the lowest of all sectors at 0.5% of stock.

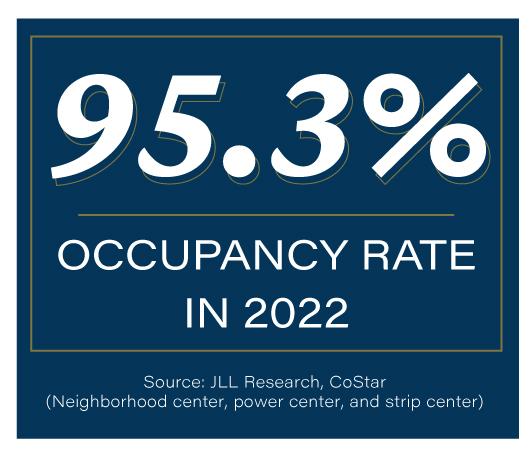

Declining retail supply has helped drive higher occupancy rates and rent growth pertaining to non-mall, multi-tenant retail, including grocery-anchored and big-box power shopping centers.

Keeping this in mind, RockStep is strategically targeting these opportunities. One case study we’ve identified is Market Heights in Harker Heights, Texas. Located within the largest Army installation in North America and anchored by Target, Dick’s Sporting Goods and Ross Dress for Less, the property has an in-going cap rate of 8.4% given the location, anchor tenants and 98% occupancy rate. As a result, the projected IRR would be 17-18% with a 1.95x MOIC.

Bridge Street Town Centre in Huntsville, Alabama, is another Core Plus strategy case study. RockStep recognizes Huntsville’s three-year population growth rate of 5.1% (seven times the national average) and a retail market rent growth of 6.4% in 2022 (top 20 in the country) as ideal factors for potential investment. Bridge Street Town Centre is anchored by the only Apple Store within a 70-mile radius, Dick’s Sporting Goods, H&M and Belk and boasts a 97% occupancy rate. The property has included “Staple On” financing in the $225mm sale that is below market and accretive to investor cash flows.

RockStep Capital is currently seeing a 7:1 ratio of retailers expanding vs. reducing their retail footprint. With RockStep Capital Fund I, we’re targeting an average yield of 14-15% IRR with 65% Opportunistic investing and 35% Core Plus investing. This strategy projects positive cash flow returns and contains an inherently lower risk compared to other asset classes.

Since 1996, our average returns have been over 35% IRR with a 2.1x MOIC. We accomplish this by targeting top 35 MSAs and assets in secondary markets. As a result, RockStep has never returned an asset to a lender or required a capital call since we’ve been in business. We’ve acquired over 9.5 million square feet of shopping centers and have over 7.5 million square feet of assets in our portfolio — 23 properties and counting.

Net-lease investment activity may continue to slow this year but, given its relatively low-risk nature, should stabilize more quickly than the broader market once more clarity emerges on the path of interest rates. Retail should be considered among the staples within the commercial real estate portfolio

Over time, retail has become relatively less risky and more profitable than other CRE assets due to low retail space availability, a decrease in new retail development and increased retail footprint within our portfolio.

With over 27 years of experience in retail real estate investment, RockStep keeps its finger on the industry’s pulse and can help you navigate it successfully. Contact us today to discuss current projects and ask about participating in RockStep Capital Fund I.

Provide your contact information below to request additional information about RockStep Fund I: