RockStep Capital has delivered above-average risk-adjusted returns through its retail investments for over two decades. Since 1996, our average returns have been a 25% IRR with a 2.1x MOIC. Considering the headwinds that malls and shopping centers have faced from the Amazon Effect and the implications of COVID-19, this track record is something we’re very proud of.

Investors often ask us how we’ve delivered these returns, having never returned an asset to a lender or required a capital call since RockStep has been in business. The answer is simple: we’re patient and only invest in assets with asymmetric returns.

Asymmetric returns are an investment profile where the potential upside returns are more significant than the potential downside returns. Further, RockStep Capital focuses on investments that generate returns with an acceptable maximum downside return. Understanding an asset’s drawbacks is critical to showing assets with asymmetric returns to our investors. Limiting potential downside performance is part underwriting discipline and part asset selection, and adhering to our underwriting principles is essential for delivering predictable returns to our investors.

RockStep must understand several items during evaluation before a mall, power center or other property is suitable for investment. The greatest source of unpredictable drops in cash flow for a retail asset is how the co-tenancy provisions in the leases are structured for the asset under evaluation.

A co-tenancy clause in a retail lease contract allows a tenant to reduce its rent if key tenants or a certain number of tenants vacate the retail space in question. A key tenant, often called an “anchor tenant,” is usually a big draw for traffic, especially in malls. It’s often one of the main reasons a tenant or group of tenants decides to be located in a specific asset.

Co-tenancy is a dangerous risk for a retail property, as the landlord essentially takes on the current and future operating risk for an anchor or group of anchors. Underestimating this risk may result in the vacancy of the anchors in question. It can also expose the asset to a group of tenants who can, at best, reduce their rent significantly or, worse, allow them to vacate upon meeting certain criteria. In either scenario, the asset’s cash flow will decrease while losing its anchor tenant and competitive standing in the market.

At RockStep Capital, we refuse to accept this risk. We understand the risk of department stores is difficult to judge. Often, the landlord doesn’t have the opportunity to assess the store’s profitability. However, RockStep will evaluate potential investments where an asset’s co-tenancy risk has already transpired. In this case, an anchor has already vacated, and the lease provisions have allowed the affected tenants to reduce their rent or leave. Therefore, the asset will generate better cash flows than underwritten because the asset’s co-tenancy has already played out.

A second source of underwriting that presents our investors with asymmetric returns is our treatment of vacancy. RockStep doesn’t “lease up” vacancies in our underwriting proformas. The result of this approach is that if we purchase an asset with vacancies and a space becomes leased, the generated profit falls to the bottom line and creates positive returns for our investors. In this case, a positive outcome for a vacant space can only expose an investor to positive cashflows.

The last underwriting rule that will expose investors to upside scenarios is our strict attention to investment basis. RockStep will only purchase a property producing enough net operating income to cover its expenses. This rule allows the basis of the company’s assets to stay as low as possible, allowing an eventual sale of the property to solely generate upside scenarios.

Although distressed assets often sell for pennies on the dollar, investments in properties that can’t pay their monthly expenses may create misalignment between the investment manager and its investors.

In these situations, the investment in the property grows each month as it fails to meet its monthly obligations. As a result, the investor must add to its investment to keep the property afloat. This forces the investment manager to make better decisions for the short term rather than the long-term health of the asset.

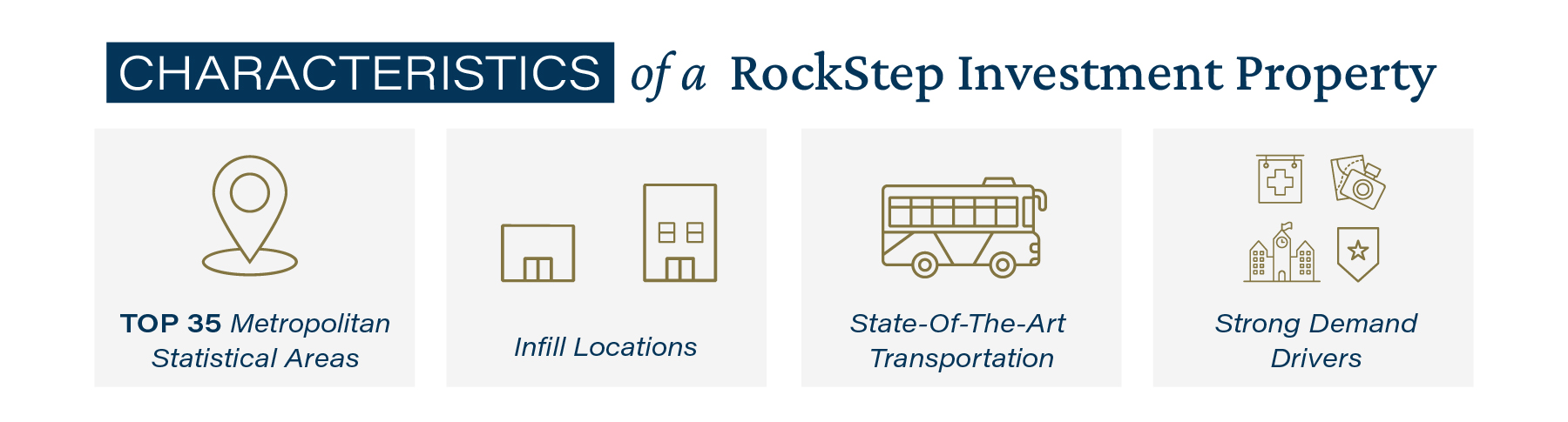

Adherence to asset selection criteria is just as important as our underwriting methodology in creating asymmetric returns for our investors in reducing risk for investors. RockStep Capital will only consider investing in properties that possess a few of the following characteristics:

- Located in one of the top 35 Metropolitan Statistical Areas (MSAs)

- Infill locations

- State-of-the-art transportation

- Strong demand drivers, including:

- Division I, II, & III universities

- Major government/military institutions

- Strong tourism

- Top 250 hospital networks

- Fortune 1000 companies

If an asset possesses many of these requirements, the property will generally be immune to economic downturns.

RockStep Capital has delivered asymmetric returns to its investors for over 25 years. Although the retail landscape is challenging, our underwriting and asset selection methodology reduces risk. It allows RockStep to offer investors return profiles that display upside scenarios far greater than downside ones. Due to our investment thesis, RockStep Capital has outperformed other retail investment managers without exposing our investors to significant risk.

Interested in learning more about investing with RockStep?

Share your contact details below to download our white paper and speak with an expert today.